There is a version of the Internet that no one builds, no one visits on purpose, and no one writes about: the tens of millions of domains whose only job is to display a registrar's template while they wait to be sold, renewed, developed, or forgotten. Where the Web Moves measured this parked web at two points in time and found it had grown from 15% to a quarter of all website records. Two points make a line; they don't make a story. This time we measured every month.

The conventional wisdom says domain parking is dying, and the conventional wisdom has receipts: between 2024 and February 2026 Google dismantled its parked-domain ad feeds — the lineage the industry still calls AFD, "AdSense for Domains," long since folded into the Search Partner Network — Team Internet's Search division lost 84% of its EBITDA in a year, Sedo's quarterly revenue fell 66%, and Bodis, one of the oldest dedicated parking platforms, shut down outright on January 31, 2026. If parking pages can no longer earn, the waiting room of the Internet should be draining.

It isn't — or rather, it only just started. The parked web doubled in size during precisely the years its revenue model was being dismantled, and only stopped growing in the quarter the last ad feed died. The lot and the money it was supposed to earn turn out to be two nearly independent systems.

We classified the website record (bare-apex A record, else www) of every resolving domain in 26 crawl snapshots from April 7, 2023 to June 9, 2026 — 176.5 million apexes at the start, 296.8 million at the end — against the same IP-to-ASN map and verified front-door registry used in Where the Web Moves, extended by a month-by-month audit that caught the front-door IPs the two-endpoint study never had to see: Bodis rotated its primary lander IP roughly monthly, GoDaddy passed estates through transitional anycast addresses, and HugeDomains' inventory spent two years on an unlabelled twelve-IP fleet. Russian-administered TLDs are excluded throughout, per project policy.

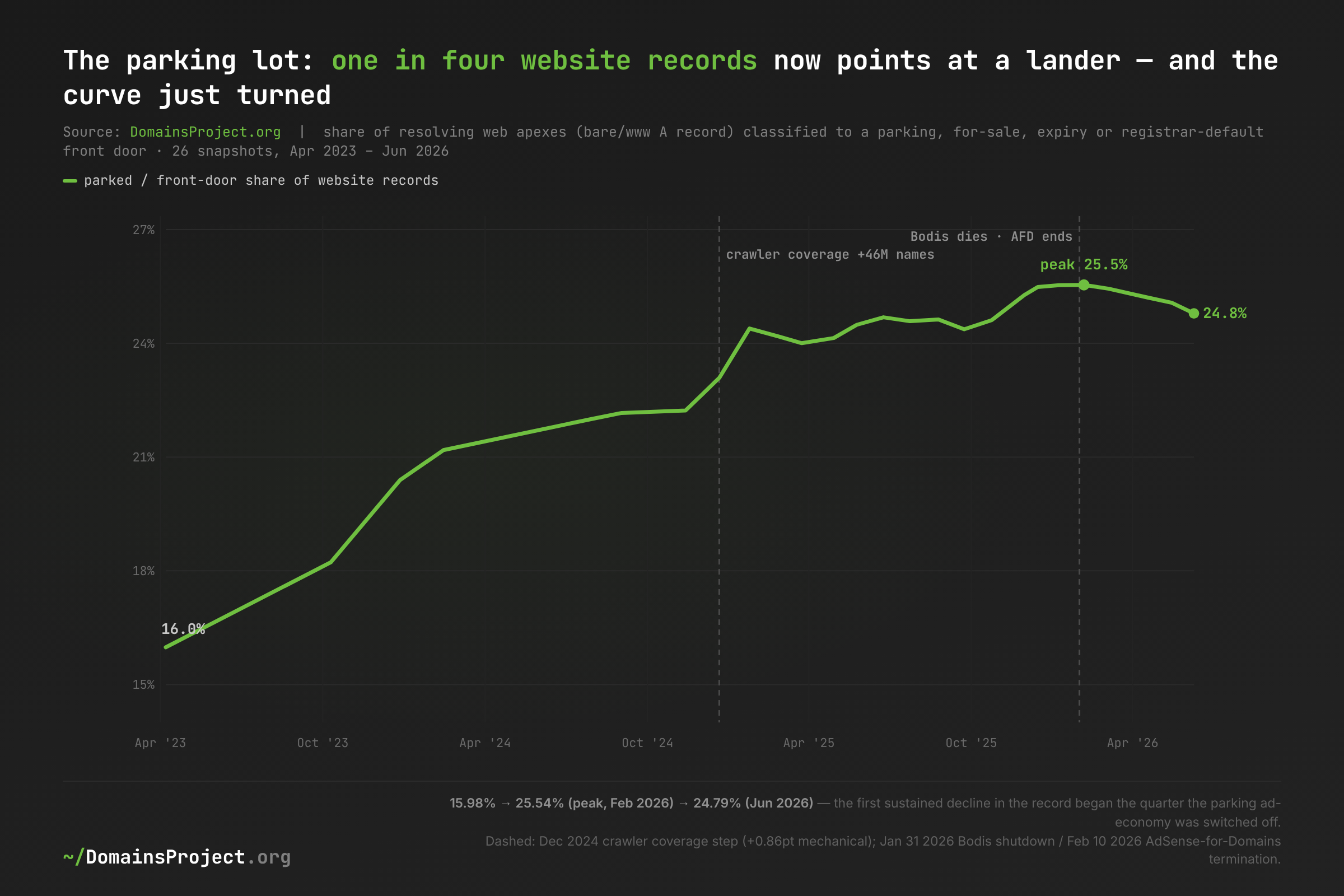

The parked web grew from 16.0% of website records in April 2023 to a peak of 25.54% on February 5, 2026 — 73.4 million domains — and then declined for four consecutive months, to 24.79% in June 2026. The peak landed five days after Bodis shut down and five days before Google's parked-domain ad feed formally ended. And the growth was never existing websites lapsing into parking: a fixed cohort of the April 2023 web shows a flat parked share from mid-2024 onward. The lot grew because the marginal web — names new to the Internet — arrives already parked.

The Data

| Dimension | Value |

|---|---|

| Snapshots | 26, April 7 2023 → June 9 2026 (monthly from Dec 2024; 2–6 month spacing before) |

| Universe per snapshot | Every apex with a website record: bare-apex A record, else www A record |

| Scale | 176,499,563 apexes (Apr 2023) → 296,843,123 (Jun 2026) |

| Classification | Empirical /24→ASN map (5.16M prefixes, 69,683 ASNs) + 91 individually verified front-door IPs |

| Parking tier | 18 operators, identical set to Where the Web Moves |

| Peak | 73,388,797 parked domains = 25.54% of website records, Feb 5 2026 |

| Exclusions | Russian-administered TLDs; Fortinet DNS-filter sinkhole (quarantined separately) |

The tier counts domains whose website record answers from a verified parking, for-sale, expiry, or registrar-default front door: GoDaddy's lander/default/Afternic/CashParking estates, Sedo, HugeDomains, Bodis, Team Internet/ParkingCrew, Trellian/Above, Hostinger parking, Dynadot, Porkbun, Namecheap and Newfold expiry landers, and kin. It does not attempt content classification: we label what the infrastructure is, not the intent of every owner behind it.

Methodology

The website record. For each apex we take the bare-apex A record if present, else www. A domain with neither is absent from that snapshot's universe. This is deliberately the same definition as Where the Web Moves, whose two endpoints are this series' first and last points.

The parking tier. A domain is "parked" in a given month if the majority of its first six website-record IPs classify to one of the same 18 operators used in #95 — no operator was added or removed for this study. Verified exact-IP front doors take precedence over the /24→ASN layer, because a single anycast address like 3.33.130.190 fronts tens of millions of domains and its announcing network (Amazon) says nothing about who operates it (GoDaddy).

The extended front-door registry — and why the endpoints moved. A monthly series is far more demanding than two endpoints: an operator that rotates its lander IP is invisible at the endpoints and a crater in the middle. Auditing every snapshot's top-500 IPs and fingerprinting suspects against adjacent months (where did these exact domains sit thirty days earlier?) added 31 labels — every one an address fix for an operator already in the tier, most confirmed by tracking sample domains into that operator's labelled IPs: five Bodis rotation IPs inside 199.59.243.0/24; four GoDaddy transitional anycast IPs; the fourteen-IP NameBright/HugeDomains fleet (nsg1/nsg2.namebrightdns.com) whose survivors moved onto HugeDomains' labelled addresses in August 2025; Hostinger's default-page IP 84.32.84.32, whose 1.65M-domain estate moved wholesale onto Hostinger's dedicated parking IP in March 2026; Team Internet's unmapped AS61969; and a Trellian lander on Hetzner. Under the extended registry the April 2023 endpoint is 15.98% parked, versus the 15.04% published in #95 (chiefly the HugeDomains fleet, already 1.2M domains in 2023); the June 2026 endpoint is 24.79% versus 24.77%. The published endpoint numbers were correct under their registry; the extended registry is strictly more complete, and the correction shrinks to +0.02 points by 2026 when every estate sits on labelled addresses.

The December 2024 coverage step. Between the November and December 2024 crawls the corpus grew from 161.3M to 207.4M website records as the crawler's known-name universe expanded. The 46.1M newly visible domains were 26.1% parked — richer in landers than the incumbent web — which mechanically added +0.86 points to the global share in one month. We do not treat that as real-world growth. The honest decomposition of the total +8.81-point rise: +6.25 points organic before the step, +0.86 mechanical, +1.70 organic after it — and every chart in this post marks the step. The closed-cohort analysis below is immune to it by construction.

What deaths can and cannot explain. Parked domains disappear from the web at almost exactly the population rate (36.4% over 38 months, versus ~37.5% for non-parked survivors of the same cohort). Near-identical mortality cannot move the parked share — so the rise is driven by what enters the web, not what leaves it.

Known limitations. (1) The audit floor is ~250K domains per snapshot: an unlabelled front door smaller than that can hide inside "Amazon AWS" or "Other" — each such miss is worth at most ~0.1 points. (2) Operators deliberately excluded to keep the tier identical to #95: united-domains' default webspace (~0.3–0.5M), Tucows/Hover defaults (~0.4M), CSC brand-protection landers (~0.6M), Network Solutions and Bluehost placeholders. (3) The 18 operators are the large western platforms; regional or bespoke parking systems — Chinese-market platforms in particular — are invisible to the tier. Together with (1) and (2), the published share is a floor, not a census. (4) The corpus itself is known-names-only, and the December 2024 step is the proof that its coverage has edges; that is exactly why the step is decomposed rather than hidden. (5) GoDaddy's "default" estate includes live Website Builder pages alongside true parking; DNS cannot split them. (6) from-absent inflow conflates newly registered, newly crawled, and returned-from-dead names; we only interpret it in stable-coverage intervals. (7) Snapshots before December 2024 are 2–6 months apart; monthly resolution begins there.

Reproducibility. A Go extractor (validated byte-identical against the #95 pipeline) reduces each crawl to per-apex website records; a single-pass Go classifier reproduces the published #95 shares exactly at both endpoints under the original registry before any extension was applied. Chart data: share series, operator series, GoDaddy estate, cohort fate, TLD panel.

The Scorecard

| Month | Website records | Parked | Share | Phase |

|---|---|---|---|---|

| Apr 2023 | 176.5M | 28.2M | 15.98% | climb |

| Dec 2023 | 198.4M | 40.5M | 20.39% | climb |

| Sep 2024 | 168.2M | 37.3M | 22.16% | climb (shrinking web) |

| Dec 2024 | 207.4M | 47.9M | 23.09% | coverage step (+0.86 mech.) |

| Jan 2025 | 244.1M | 59.5M | 24.39% | plateau begins |

| Sep 2025 | 279.1M | 68.0M | 24.37% | plateau |

| Feb 2026 | 287.3M | 73.4M | 25.54% | peak |

| Jun 2026 | 296.8M | 73.6M | 24.79% | decline (4th consecutive month) |

Download: parkinglot-share.csv

The curve has three acts, and the act breaks line up with the ad-economy's demolition schedule. The climb (Apr 2023 – Jan 2025, +8.4 points) happened while parking still paid. The plateau (Feb – Oct 2025, 24.0–24.7%) coincides with Google opting existing advertisers out of parked-domain inventory from March 19, 2025 and purging the last high-value advertisers that September. The final push to the peak and the turn (Nov 2025 – Jun 2026) bracket the terminal events: Bodis shut down January 31, 2026; Google's parked-domain feed formally ended February 10; our peak is the February 5 crawl. Data → inference: the timing is consistent with parking economics driving the flow of domains into the lot with a lag — money stopped arriving in 2025, growth stopped in 2026. We observe coincidence in time, not proven cause; but the sequence repeats at operator level (below), which is harder to dismiss.

Concentration

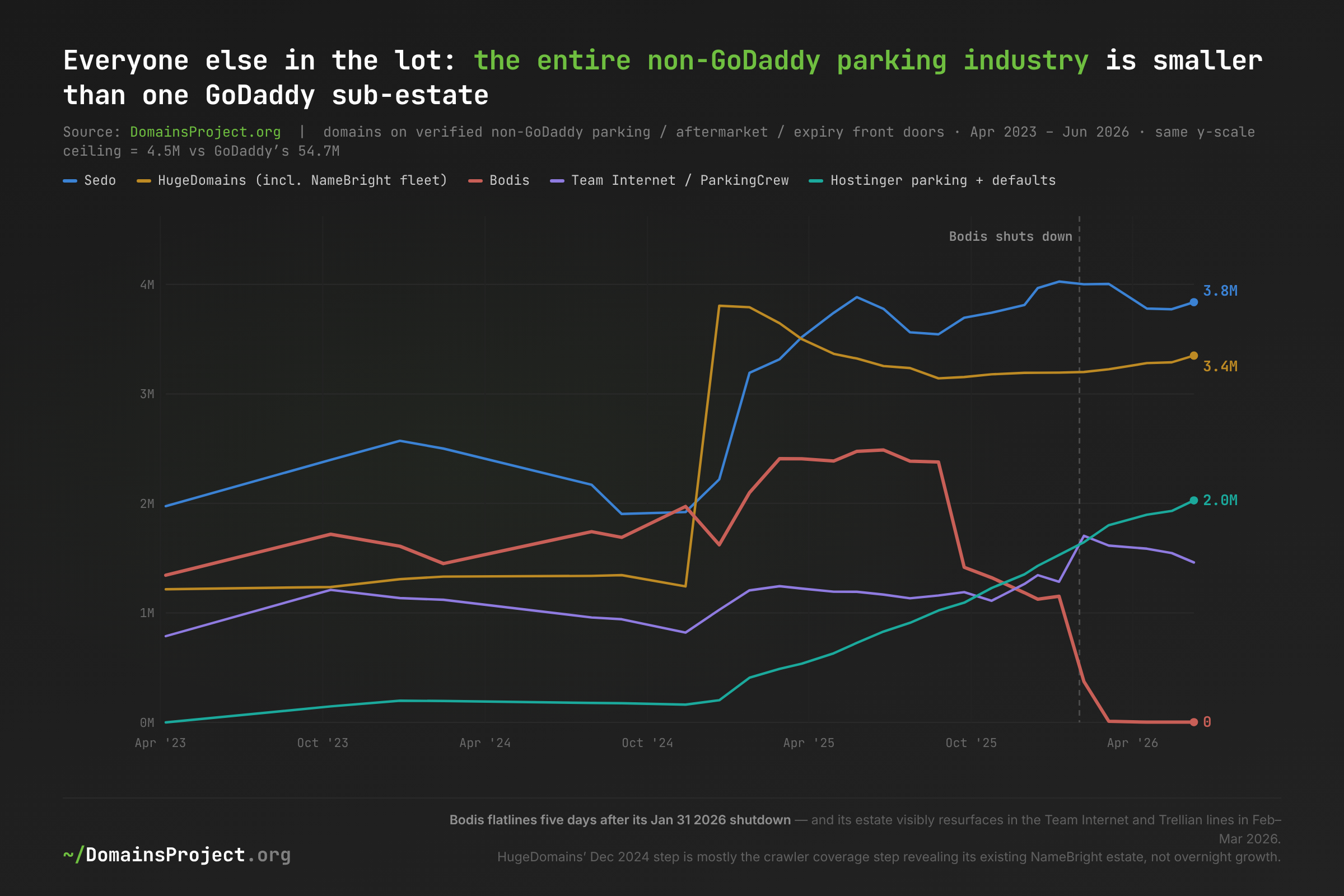

| Operator (June 2026) | Domains | Share of the lot |

|---|---|---|

| GoDaddy front doors | 54.7M | 74.3% |

| Sedo | 3.8M | 5.2% |

| HugeDomains (incl. NameBright fleet) | 3.4M | 4.6% |

| Hostinger parking + defaults | 2.0M | 2.8% |

| Confluence/PDR | 1.7M | 2.3% |

| Trellian/Above | 1.6M | 2.2% |

| Team Internet / ParkingCrew | 1.5M | 2.0% |

| Bodis | 0 | dead |

| Everyone else (10 named operators) | 4.9M | 6.6% |

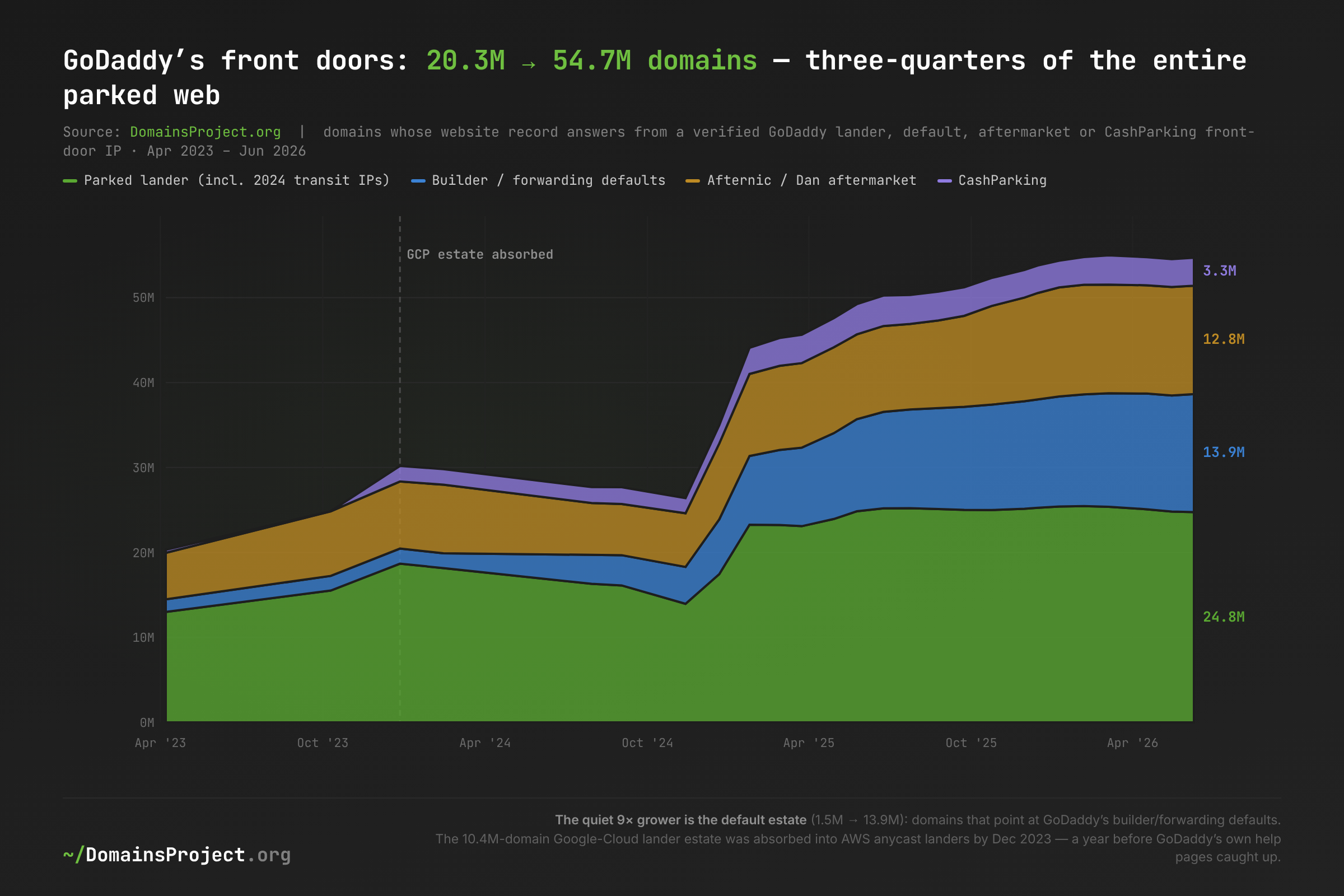

Three-quarters of the parked web points at one company's front doors, throughout the entire series. GoDaddy's estate never dips below 72% of the tier. Whatever happens to parking as an industry is, to first order, whatever GoDaddy decides to do with 54.7 million domains.

GoDaddy: The Landlord's Landlord

| GoDaddy sub-estate | Apr 2023 | Jun 2026 | Change |

|---|---|---|---|

| Parked lander | 13.00M | 24.75M | 1.9× |

| Builder / forwarding defaults | 1.48M | 13.89M | 9.4× |

| Afternic / Dan aftermarket | 5.48M | 12.76M | 2.3× |

| CashParking | 0.35M | 3.29M | 9.4× (via an Oct 2023 rebuild) |

| Total front doors | 20.31M | 54.69M | 2.7× |

Download: parkinglot-gd-estate.csv

The quiet story is the default estate: 1.48M → 13.89M domains, still growing in 2026 — and it earns no parking-ad revenue at all. These are names pointing at GoDaddy's builder and forwarding defaults — a registration that came with DNS pre-pointed at GoDaddy infrastructure and never went anywhere else. That matters for the causal story: the 2026 contraction is concentrated in the ad-monetized estates (the parked lander shed 0.7M domains between February and June 2026, Bodis's 1.15M went to zero), while the never-monetized default estate kept growing (+0.7M over the same months). The lot's decline has exactly the shape an advertising shock predicts — and its remaining growth has exactly the shape unconfigured registrations predict. The aftermarket estate more than doubled across exactly the window in which GoDaddy re-engineered its commissions to force inventory onto its own landers (the February 2023 realignment: 15% with Afternic landers, 25% without; raised to 20%/30% with September 2024's "Afternic Boost"), migrated Dan.com's inventory and closed Dan.com in June 2025.

The monthly series also re-dates a migration we could only bracket before. In #95 we reported GoDaddy's lander estate moving from Google Cloud to AWS anycast somewhere inside a 38-month window; public evidence (GoDaddy's own help pages on the Wayback Machine) suggested 2024–2025. The DNS record says otherwise: the 10.4M-domain Google Cloud estate was 85% gone by October 2023 and fully absorbed by December 2023. GoDaddy's documentation continued instructing users to point domains at the Google Cloud IP for at least another year — and ~50K domains still pointed at those retired GCP addresses in 2026, a residue that actually grew in late 2024 while the documentation still listed the old IP. Hand-configured A records copied from stale docs are the most parsimonious explanation we can offer; whatever those addresses serve today, the domains left GoDaddy's managed estate, and at 0.02% of the universe they do not move any number in this post.

Everyone Else: A Succession War in a Shrinking Kingdom

Download: parkinglot-families.csv

Bodis's death is the sharpest event in the series — and the market's response is visible in aggregate within one month. Bodis fronted 1.3–2.5M domains for 33 straight months (rotating its primary lander IP almost monthly inside its /24, which is why a two-endpoint study could never see it). Its estate fell to 372K within five days of the January 31, 2026 shutdown and to zero by March. In February–March 2026, Team Internet's line jumps +420K and Trellian's +200K — and fingerprinting confirms those are literally ex-Bodis domains re-pointed at the successors' landers. The Landlords of the Web framing holds to the end: when a landlord dies, the tenants get reassigned, not freed.

HugeDomains was never absent — we just couldn't see it. #95 reported HugeDomains as an operator that "did not exist in our 2023 measurement." The monthly audit found its inventory sitting, from April 2023 onward, on a twelve-IP round-robin EC2 fleet tied to NameBright (TurnCommerce's registrar arm) — 1.2M domains in 2023, 3.8M at the December 2024 peak — before consolidating onto HugeDomains' labelled addresses in August 2025. The correction is a caution for every IP-based census, including ours: an aftermarket giant hid inside "Amazon AWS" for two years.

Sedo's inventory grew 1.97M → 3.84M while its revenue fell 66%. More shelf space, less money per shelf: parked inventory and parking revenue are separate systems. IONOS is divesting Sedo as a discontinued operation while its lot is the fullest it has ever been.

Hostinger built a parking system during the funeral. Hostinger's default-page estate grew from ~150K (2023) to 1.65M (February 2026), then moved wholesale onto a dedicated parking IP in March 2026 — the infrastructure formalization of a parking business launched in the quarter the Google feed died, presumably aimed at the post-Google monetization stack (RSOC, Yahoo feeds, affiliate landers).

Composition, Not Conversion: Who Actually Fills the Lot

The single most important analytical result in this study comes from holding the population fixed. Take every domain that had a website record in April 2023 and follow only those.

| Apr 2023 | Sep 2024 | Jun 2026 | |

|---|---|---|---|

| Cohort still present | 176.5M | 130.1M | 110.8M |

| Parked share within the cohort | 15.98% | 18.48% | 18.33% |

| Whole-web parked share | 15.98% | 22.16% | 24.79% |

The April 2023 web converted into parking for about fifteen months (+2.4 points) and then stopped; everything after mid-2024 is composition. The cohort's parked share is flat at 18.2–18.6% for two full years while the whole-web share climbs another six points. The difference is the inflow: in stable-coverage intervals, 2–3M domains enter the lot each month from outside the previous month's web (new registrations and re-registrations arriving pre-parked), roughly 2M convert from live infrastructure, ~1M un-park, and ~3M die. The lot is not a warehouse; it is a high-throughput machine whose intake happens at the registration desk. Implication: the parked share of the web is largely a property of what gets registered, not of what webmasters abandon — which is why it tracks registration economics (promo pricing, speculation waves, aftermarket commission design) rather than website economics.

Download: parkinglot-fate.csv

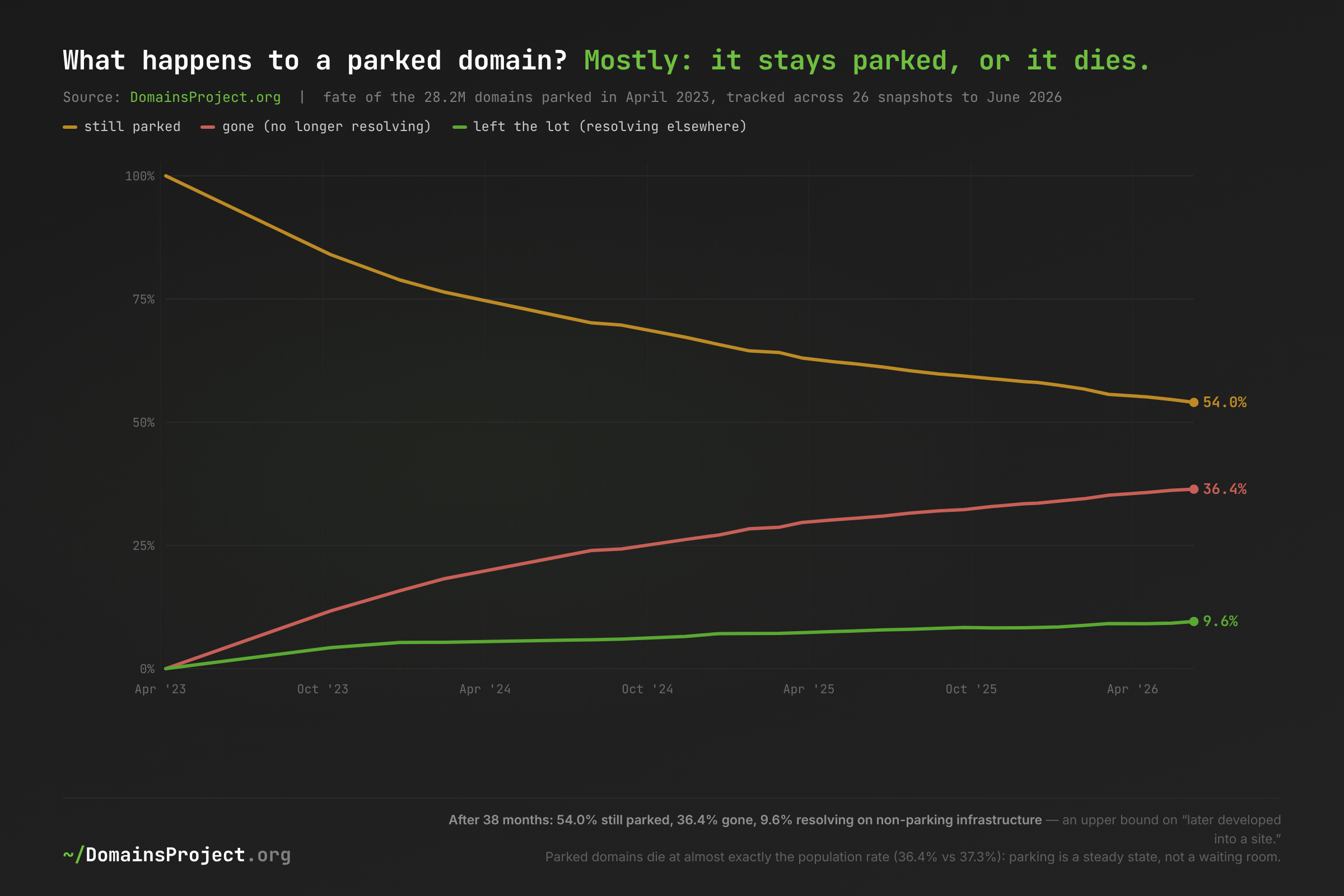

A parked domain's three-year fate: 54.0% still parked, 36.4% dead, 9.6% anything else. That 9.6% — domains that left the lot for non-parking infrastructure — is an upper bound on "eventually developed into a website," since it includes moves to hosting defaults and other placeholders. And parked domains die at almost exactly the population rate (36.4% vs 37.3%). Parking is not a waiting room before development and not a hospice before death; it is a stable end-state with ordinary mortality and a graduation rate below one in ten per three years.

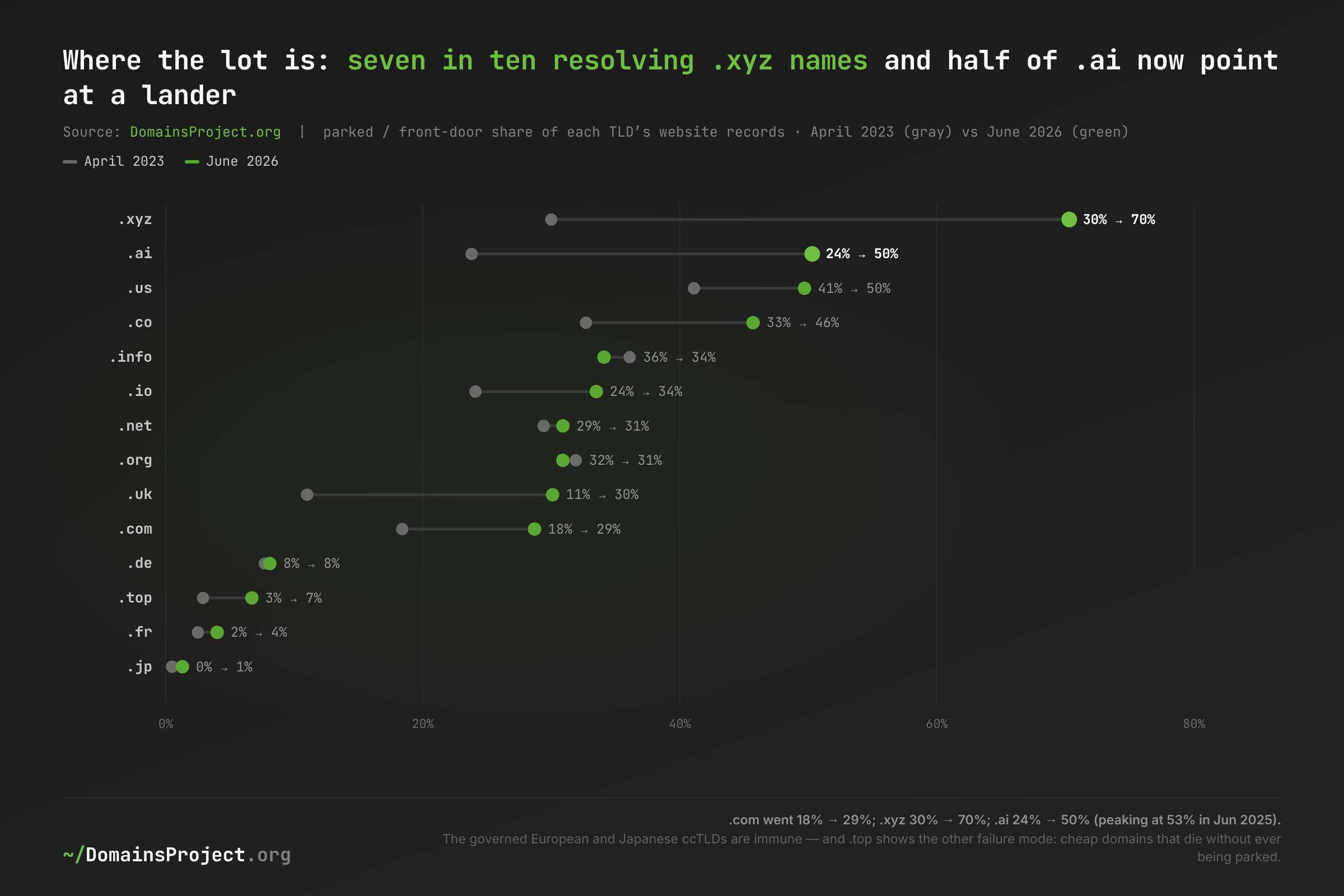

The Geography of the Lot

Download: parkinglot-tld.csv

Seven in ten resolving .xyz names now point at a lander (30% → 70%), and half of .ai does (24% → 50%, peaking at 53% in June 2025). The .ai figure is consistent with what our .ai gold-rush analysis found from registration data — a parked name is not proof of speculative intent, but half a namespace pointing at for-sale infrastructure is the shape speculation leaves. .us (50%), .co (46%) and .uk (11% → 30%) tell the same story at national scale, and .com — the reference namespace — went 18.4% → 28.7%.

The exceptions define the rule twice over. The governed ccTLDs are immune: .jp at 1.3%, .nl at 3.3%, .fr at 4.0%, .de at 8.1% — registries with identity verification, meaningful pricing, and low speculation simply do not fill with landers (the same registries that top every survival table). And .top, the churn-belt archetype, measures parked at only 6.7%. One reading — a hypothesis our infrastructure data can suggest but not prove — is that its largely Chinese-market registrants monetize outside the western platforms our registry covers; it is equally a limitation, since any Chinese-market parking systems would be invisible to our 18-operator tier. Either way, the observable fact stands: cheap .top domains die without ever passing through the western lot.

What's at Stake

- Every "number of websites" statistic is inflated by a quarter, and the error is not random. 73.6 million resolving domains render a few dozen lander templates. Crawler operators, LLM training pipelines, and market sizings that count resolving domains as sites are counting GoDaddy's inventory management system tens of millions of times — and the error grew eight points in three years, so any trend built on raw counts inherits it.

- The lot is one company's balance sheet decision. At 74% concentration, a single GoDaddy policy change — a commission tweak, a default-page redesign, an estate migration — moves the measured web more than the entire non-GoDaddy parking industry combined. Its 2023 GCP→AWS move rewrote "where the web is hosted" statistics by whole percentage points without a single customer acting.

- Parking infrastructure is where expired trust goes to be resold. More than a third of today's lot is expiry and aftermarket inventory: domains with years of residual reputation, backlinks, and stale references now answering from anycast IPs that rotate operators. Security systems that treat "domain still resolves" as continuity inherit 73 million counterexamples.

- The post-AFD contraction is real but young. Four months of decline (−0.75 points) after 34 months of growth, with the parked count stalled at ~73.5M against a growing web. Bull case for the lot: RSOC, Yahoo feeds and affiliate landers replace enough revenue to hold inventory (Hostinger is betting this way). Bear case: marginal renewals lapse without even ad pennies and the lot drains into the dead web over the 2026–27 renewal cycles — though the record so far lends this little support: parked domains died at population rates even while parking revenue collapsed through 2025, so renewal behavior has yet to show any ad-revenue sensitivity. Base case, on this data: a slow leak driven by reduced intake, not an exodus — new-name inflow has slowed, but the stock is sticky.

What Would Help

1. Registrars and parking operators: label the estates. Namecheap's expiry landers announce themselves in reverse DNS (parklogic.net); almost nobody else's do. A reserved rDNS convention or a _lander TXT record would let every crawler, security vendor, and researcher separate inventory from publication without heuristics. The information is not secret — it is just unpublished.

2. Measurement researchers: treat front-door IPs as first-class, rotating infrastructure. The difference between our published endpoints (15.0% → 24.8%) and the audited monthly series (16.0% → 24.8% with a 25.5% peak) is thirty-one IP labels found by fingerprinting adjacent snapshots. A two-endpoint study cannot see an operator that rotates addresses monthly; a maintained public registry of parking front doors — with history — would improve every downstream census, including ours.

3. Anyone counting websites: subtract the lot, and say so. Netcraft's survey counts ~1.43 billion "sites" and ~201 million active ones; our tier explains a large slice of the gap at the resolving-domain level. Publishing parked-share alongside domain counts should be as standard as seasonally adjusting economic data.

4. Security vendors: expiry landers are a temporal trust boundary. A domain's move onto a verified expiry/aftermarket front door is a machine-readable signal that its prior identity ended — stronger and earlier than WHOIS changes. Our per-snapshot classification tables make that transition observable at monthly resolution; use registrar-published labels (see #1) to make it real-time.

5. Registries: the .xyz number is a governance choice. A namespace where 70% of resolving names point at landers is the endpoint of pure-volume registration economics. The governed ccTLDs at 1–8% demonstrate the alternative exists at scale — and they also top every survival and stability table we publish. Both models are legitimate businesses; only one produces a namespace that is mostly real.

Methodology: 26 DNS crawl snapshots (April 7, 2023 – June 9, 2026) reduced to per-apex website records (bare-apex A record, else www; ICANN public-suffix apex; one domain, one vote); classification by empirical /24→ASN map plus 91 verified front-door IPs with exact-IP precedence; parking tier fixed to the 18 operators of Where the Web Moves; Russian-administered TLDs excluded. Endpoint results reproduce the published #95 numbers exactly under the original registry; the extended registry and all deltas are documented above. Cohort and flux analyses use per-snapshot classification tables joined on apex. External timeline: Google Ads parked-domain policy changes 2024–2026, Bodis shutdown notice (Jan 28, 2026), Team Internet and United Internet filings, Verisign DNIB. Explore the dataset behind this analysis at domainsproject.org/dataset or browse per-TLD statistics.