Updated 23 June 2026 — refreshed against the June 2026 dataset snapshot (4,132,471 observed .ai hostnames, up from 3.45M) and triangulated against our 9 June 2026 typed-DNS crawl. The original March 2026 edition predated our data-journalism format standard and our first-party DNS resolution data. This revision adds a full Methodology section, updates every dataset-derived figure, adds an A-record resolution pass that tests how many .ai domains actually answer in DNS, and tempers the "subdomains equal real infrastructure" reading now that the data shows a large share of those subdomains are hosting-panel boilerplate. External market figures — Anguilla's revenue, aftermarket sales, pricing — are as of the original publication and are dated inline. A dedicated June 2026 follow-up — ".ai After the Gold Rush: 94% Resolve, Half Show No Real Use, and 9% Are For Sale" — extends this DNS work to the full root population across A, MX, NS, and TXT records, measuring how many .ai domains actually do anything.

Anguilla is a flat coral island in the eastern Caribbean. It has 14,000 residents, no direct flights from the US mainland, and a GDP smaller than a mid-tier Series B round. It also holds the two most valuable letters in the domain name system.

The .ai country-code TLD was delegated to Anguilla in the mid-1990s, back when "artificial intelligence" was an academic discipline, not a market category. For nearly two decades, .ai was an afterthought — fewer than 50,000 registrations as recently as 2018. Then the AI boom happened. ChatGPT launched in November 2022, venture capital flooded into anything with "AI" in the pitch deck, and founders discovered that a two-letter domain extension could do what no marketing budget could: make a company sound like it was born for this moment.

By January 2026, .ai crossed one million registered domains. Anguilla's government earned an estimated $93 million from .ai registration fees in 2025 — roughly 47% of total government revenue, up from less than 1% before the boom. Premier Cora Richardson Hodge's 2026 budget address confirmed: "Revenue from domain name registration continues to exceed expectations," with receipts forecast to hit EC$260.5 million (~$96.4 million) for 2026.

We analyzed 4.13 million observed .ai hostnames in the DomainsProject dataset — 1.17 million distinct root registrations and 2.97 million subdomains — and cross-referenced the data with registry figures, aftermarket sales records, government revenue disclosures, and Anguilla's own budget documents.

The headline: .ai is a durable trend with a speculation problem on top — and the speculation is getting more expensive. The adoption signals are real: over 30% of recent Y Combinator AI startups use .ai as their primary domain, and our dataset shows 1,202 .ai domains running 100+ subdomains each — production platforms, not parked pages. But the froth is real too. A large share of subdomains turn out to be auto-generated hosting-panel boilerplate rather than product infrastructure; external audits put placeholder .ai sites around 61%; aftermarket prices have surged 13x in two years; Anguilla raised wholesale registration fees by $20/year in March 2026; and Spamhaus now flags .ai in its Top 20 worst TLDs for the first time. The foundation is sound. The costs of both the foundation and the froth are rising.

The Data

DomainsProject continuously crawls and indexes domains across every delegated TLD in the IANA root zone. Here's what we observe for .ai and comparable tech-oriented TLDs:

| TLD | Type | Hostnames in Dataset | Rank | Global Share |

|---|---|---|---|---|

| .io | ccTLD (British Indian Ocean Territory) | 13.8M | #28 | 0.43% |

| .app | gTLD (Google Registry) | 6.7M | #51 | 0.21% |

| .dev | gTLD (Google Registry) | 4.4M | #70 | 0.14% |

| .ai | ccTLD (Anguilla) | 4.13M | #72 | 0.13% |

| .tech | gTLD (Radix) | 4.1M | #73 | 0.13% |

Dataset counts reflect observed hostnames — including subdomains — seen via active DNS crawling, not registry registration figures. This means dataset figures run larger than registry-reported counts: .ai shows 4.13M observed hostnames (1.17M distinct root registrations plus 2.97M subdomains) versus approximately 1 million registry registrations as of January 2026. We use dataset figures for cross-TLD comparison and registry figures for .ai-specific trend analysis throughout this post. (.ai has slipped from #67 to #72 in the global ranking not because it shrank — it grew 20% — but because several promotional gTLDs grew faster.)

Methodology

This post mixes our first-party dataset with external market data, so it is worth being precise about what each number means.

- Observed hostname (FQDN). Our base unit: a fully-qualified name seen in our crawl —

name.ai,www.name.ai, andapi.name.aiare three hostnames under one registrable domain. Per-TLD totals (the 4.13M) are deduplicated observed hostnames, not registrations. - Root registration / apex. A registrable

name.aidomain. .ai is a flat namespace (no second-level registry suffixes), so the apex is always the last two labels. We count 1,171,566 distinct apexes; 1,158,046 of them were also seen as a barename.aihostname, and the rest were observed only through a subdomain. - Subdomain. Any observed hostname with depth greater than two (

app.name.ai). We classify subdomains by their leftmost label. - Production-service vs. hosting-panel subdomains. A correction from the original edition: not all subdomains indicate a team building infrastructure. Prefixes like

api,app,dev,staging, anddashboardare production-service signals. Prefixes likecpanel,webmail,webdisk,autodiscover, andwwware hosting-panel boilerplate — auto-provisioned by shared-hosting control panels whether or not anyone uses them. We separate the two below, because conflating them overstates "real infrastructure." - Resolution. In the triangulation section, an apex resolves if our 9 June 2026 A-record crawl returned

NOERRORwith at least one IP. This is our first-party measure of "active vs. placeholder," independent of the external audits the original post relied on. - Buzzword, sector, and saturation counts are computed on the apex second-level label by prefix match (e.g.

agent*), are not mutually exclusive, and are validated by spot-checking samples. They describe naming intent, not verified business activity.

Known limitations. A snapshot, not a time series — registration trends in this post come from registry disclosures, not from our single crawl. Subdomain visibility is biased by hosting setup (cPanel hosts expose a fixed boilerplate set; serverless/edge deployments expose almost none), so subdomain counts undercount modern stacks and overcount shared hosting. Keyword classification is heuristic. External figures (Anguilla revenue, aftermarket prices, Spamhaus rankings) carry their sources' own dates and caveats, noted inline. Apex-level figures are reproducible from the .ai statistics page and the dataset.

The Scorecard: .ai's Trajectory

.io still leads the tech TLD pack at 13.8 million observed hostnames in our dataset — about 3.3x the .ai count. But that lead is narrowing fast. .io had a 20-year head start, and its registry-reported growth has slowed to roughly 7% annually. .ai registry registrations are growing at 130%+ year-over-year. At current trajectories, .ai will surpass .io in registry registrations within 12-18 months.

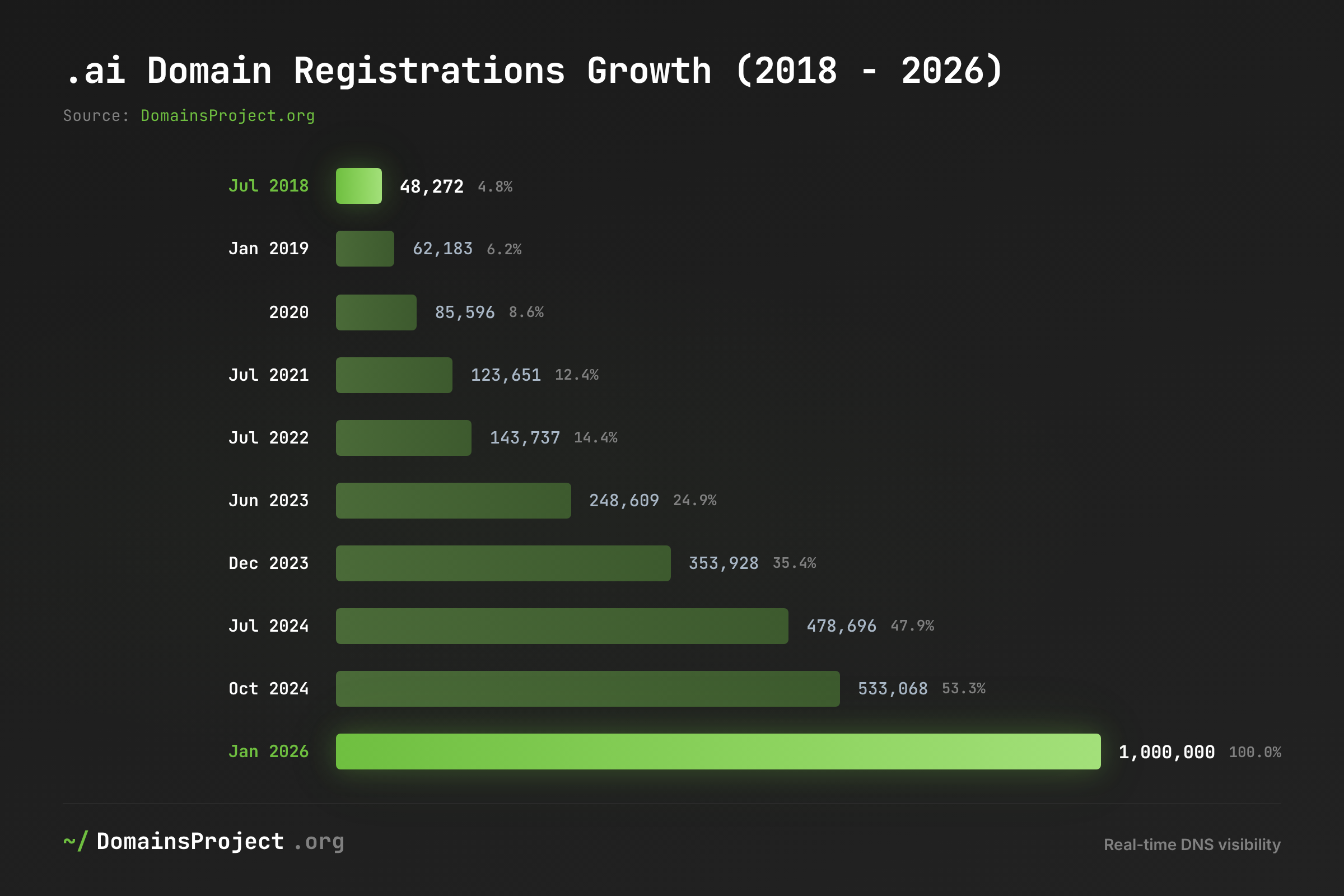

Registration Growth

| Date | .ai Registered Domains | Milestone |

|---|---|---|

| July 2018 | 48,272 | Baseline |

| January 2019 | 62,183 | |

| 2020 | 85,596 | GPT-3 launches |

| July 2021 | 123,651 | GitHub Copilot preview |

| July 2022 | 143,737 | Pre-ChatGPT |

| June 2023 | 248,609 | Post-ChatGPT surge |

| December 2023 | 353,928 | |

| July 2024 | 478,696 | AI VC funding hits $110B |

| October 2024 | 533,068 | |

| January 2025 | ~610,000 | Identity Digital takes over management |

| January 2026 | 1,000,000+ | 7x growth in 3 years |

From July 2022 to January 2026, .ai registrations grew 7x — from 144,000 to over one million. The inflection point is unmistakable: ChatGPT's November 2022 launch kicked off a registration surge that hasn't slowed. Daily additions hit 2,008 per day in January 2026 — up from 1,318 per day in 2025 — and the renewal rate sits at approximately 90% according to registry data.

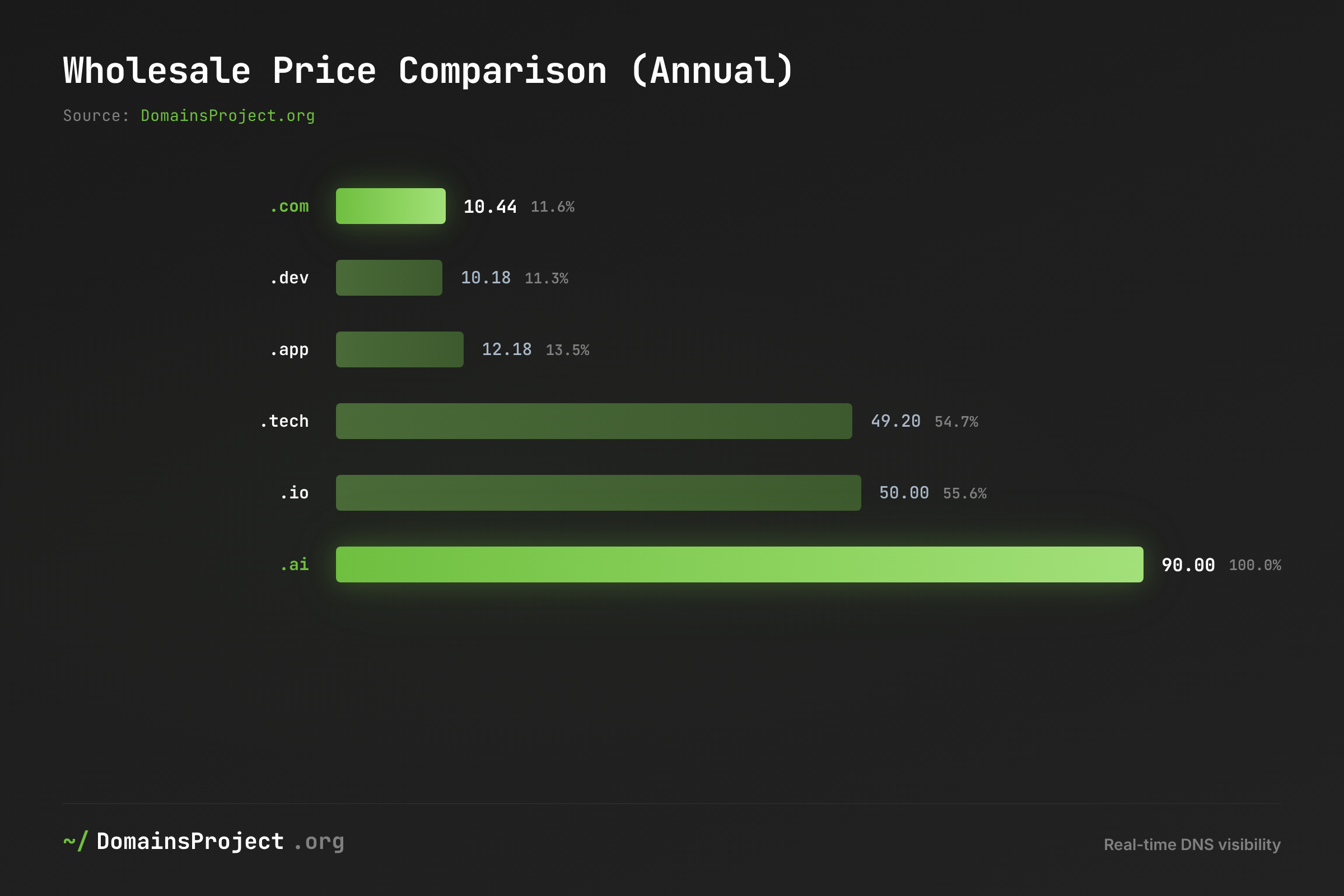

Pricing Comparison

| TLD | Wholesale Price (Annual) | Minimum Term | Effective 2-Year Cost |

|---|---|---|---|

| .com | $10.44 | 1 year | $20.88 |

| .dev | $10.18 | 1 year | $20.36 |

| .app | $12.18 | 1 year | $24.36 |

| .tech | $49.20 | 1 year | $98.40 |

| .io | $50.00 | 1 year | $100.00 |

| .ai | $90.00 | 2 years | $180.00 |

Wholesale prices via Cloudflare Registrar (at-cost). Retail prices vary by registrar, typically $100-$220/yr for .ai. The .ai price reflects a $20/yr wholesale increase effective March 5, 2026, up from $70/yr.

.ai is the most expensive mainstream tech TLD at $90/year wholesale — nearly 9x the cost of .com. And it just got more expensive. Anguilla's registry raised wholesale prices by $20/year in March 2026 — a 29% increase on the annual rate — signaling confidence in inelastic demand. Despite the premium, the 90% renewal rate suggests registrants see the cost as justified — or at least, they haven't blinked yet.

Top Aftermarket Sales

| Domain | Sale Price | Year | Buyer (if known) |

|---|---|---|---|

| bot.ai | $1,200,000 | 2026 | Undisclosed (Sedo BIN sale) |

| fin.ai | $1,000,000 | 2025 | Intercom (unconfirmed) |

| wisdom.ai | $750,000 | 2025 | Sold via Grit Brokerage |

| you.ai | $700,000 | 2023 | Dharmesh Shah (HubSpot) |

| lotus.ai | $400,000 | 2026 | Lotus Health |

| stack.ai | $258,888 | 2023 | Undisclosed |

| npc.ai | $250,000 | 2023 | Undisclosed |

| girlfriend.ai | $250,000+ | 2024 | Undisclosed |

| ace.ai | $205,000 | 2025 | Undisclosed |

The broader .ai-adjacent market is even more extreme. ai.com — not a .ai domain but the ultimate AI vanity address — sold for $70 million in February 2026, making it the most expensive domain sale ever recorded, more than doubling the previous record of $30 million for voice.com. The buyer was Kris Marszalek, CEO of Crypto.com, who debuted the site during Super Bowl LX with a personal AI agent product. The sale price was paid in cryptocurrency. The transaction underscores how "AI" as a naming signal has transcended any single TLD — and any single industry.

The .ai aftermarket exploded from $878,000 in total sales (2022) to $4.5 million (2023) to an estimated $11.7 million (2024) — a 13x increase in two years. In 2024, .ai ranked third globally in aftermarket sales volume on Afternic, with the highest sell-through rate among all top 10 TLDs. Fifteen or more .ai domains have sold for $100,000+ in 2026 alone. Bot.ai's $1.2 million sale via Sedo in February 2026 was the first publicly reported seven-figure .ai sale ever.

Inside the .ai Namespace: What 3.45 Million Domains Reveal

Registry counts tell you how many domains are registered. Our dataset tells you what people are actually building — and squatting on. We broke down all 4.13 million observed .ai hostnames to map the namespace.

Root Registrations vs. Subdomains

| Category | Count | Share of Observed |

|---|---|---|

| Apex hostnames (name.ai) | 1,158,046 | 28.0% |

| Subdomains (sub.name.ai+) | 2,974,425 | 72.0% |

| Total observed hostnames | 4,132,471 | 100% |

Behind those hostnames sit 1,171,566 distinct registrable .ai domains — the namespace has crossed 1.17 million observed roots, up from 995,445 a quarter earlier.

Nearly three-quarters of observed .ai hostnames are subdomains, not roots — but the original edition over-read that ratio. Subdomains do mean someone configured DNS, which separates .ai from a pure parking lot. They do not all mean someone is building a product: as the next table shows, a large slice of those subdomains is hosting-panel boilerplate that shared-hosting control panels create automatically. The production-service prefixes — api, app, dev, staging — are the real signal, and they are present in the hundreds of thousands.

Infrastructure Fingerprint

| Subdomain Prefix | Count | Class | What It Signals |

|---|---|---|---|

| www. | 1,109,113 | boilerplate | Standard web presence |

| api. | 87,628 | production | Production APIs |

| app. | 76,382 | production | Web applications |

| pay. | 68,780 | boilerplate | Registrar / hosting pay-link pages |

| dev. | 43,695 | production | Development environments |

| mail. | 42,190 | boilerplate | Email infrastructure |

| staging. | 27,821 | production | Pre-production testing |

| admin. | 27,550 | production | Admin dashboards |

| cpanel. | 16,923 | boilerplate | cPanel control panel |

| webmail. | 15,923 | boilerplate | cPanel webmail |

| webdisk. | 15,563 | boilerplate | cPanel WebDAV |

| autodiscover. | 11,492 | boilerplate | Outlook autodiscovery |

The cPanel fingerprint is unmistakable — and it is a caution flag, not a sign of engineering. When cpanel, webmail, webdisk, and autodiscover all appear together (as they do, in the 11,000–17,000 range each), they mark domains parked on shared hosting whose control panel mints those subdomains by default. The honest read is to separate them from production prefixes. On the production side the signal is strong: 87,628 api. subdomains, 76,382 app. subdomains, and 43,695 dev. subdomains point to real services. 1,202 .ai domains run 100+ subdomains each (164,110 subdomains in total), and another 59,018 run 10–99 (1.24 million subdomains) — these are the platforms and growing products, and there are over three times as many of them as the 358 the original edition found.

The Platforms: Who's Building Real Infrastructure

| Domain | Subdomains | Category |

|---|---|---|

| supersonic.ai | 3,544 | Marketing optimization |

| com.ai | 3,222 | Domain platform |

| robovision.ai | 3,122 | Computer vision |

| twcc.ai | 2,697 | Cloud computing (Taiwan) |

| builder.ai | 2,332 | App development platform* |

| order-online.ai | 1,671 | E-commerce |

| vudini.ai | 1,567 | Analytics |

| cognitiveclass.ai | 1,231 | Education (IBM) |

| firstlight.ai | 1,114 | Media intelligence |

| eprivacy.ai | 999 | Privacy compliance |

*builder.ai entered insolvency proceedings in 2025; its subdomains still resolve in our crawl. This is itself the lesson — a high subdomain count is a DNS snapshot, not proof of a going concern. Subdomain mass can outlive the company that built it.

The top .ai platforms by subdomain count span the full AI application stack — from computer vision and cloud infrastructure to privacy compliance and education. This is not a namespace dominated by any single use case; it's a cross-industry phenomenon. But builder.ai is the caveat in miniature: count subdomains to find where infrastructure was deployed, then verify which of it is still live before drawing conclusions — which is exactly what the DNS-resolution pass later in this post does.

Notable Companies in the Dataset

Our crawl confirms every major .ai-branded company with active subdomains — a proxy for real infrastructure deployment:

| Company | Domain | Subdomains | Infrastructure Evidence |

|---|---|---|---|

| H2O.ai | h2o.ai | 248 | ML platform (production clusters) |

| Stability AI | stability.ai | 99 | Image generation |

| Perplexity | perplexity.ai | 85 | AI search |

| Pony.ai | pony.ai | 82 | Autonomous vehicles |

| Cohere | cohere.ai | 71 | Enterprise LLMs |

| Jasper | jasper.ai | 58 | AI writing |

| Together AI | together.ai | 53 | Inference infrastructure |

| xAI | x.ai | 52 | Foundation models |

| Mistral AI | mistral.ai | 45 | Foundation models |

| Shield AI | shield.ai | 37 | Defense AI |

| C3.ai | c3.ai | 38 | Enterprise AI |

| Copy.ai | copy.ai | 31 | AI writing |

| Character.AI | character.ai | 28 | AI companions |

| Figure AI | figure.ai | 23 | Robotics |

| Notion | notion.ai | 15 | Productivity AI |

| Inflection AI | inflection.ai | 11 | Foundation models |

The big tech defensive registrations are equally telling. Google, Microsoft, Meta, Nvidia, Amazon, Tesla, Anthropic, and DeepMind all hold their .ai domains — but most are minimal deployments (1-5 subdomains). Apple and OpenAI do not appear in our dataset as .ai root registrations at all. The .ai TLD remains a startup phenomenon: the incumbents own their .ai defensively, but they don't build on it.

DNS Reality Check: How Many .ai Domains Actually Resolve

Subdomain counts measure ambition; DNS resolution measures whether the lights are on. We took every observed .ai hostname and checked it against our 9 June 2026 A-record crawl — does it still return a live IPv4 address?

| Slice | Count | Returns Live A Record | Resolution Rate |

|---|---|---|---|

| Registrable .ai roots | 1,171,566 | 1,012,993 | 86.5% |

| All observed .ai hostnames | 4,132,471 | 3,191,535 | 77.2% |

86.5% of registered .ai roots still resolve to a live address — a high figure that anchors the bull case in first-party data rather than renewal-rate inference. For comparison, our crawl puts the whole-namespace resolution rate at 58.9% and the promotional gTLDs (.shop, .online, .xyz) below 40%; .ai sits far above both. A registered .ai domain is, much more often than not, a domain someone keeps pointed at something.

But resolving is not the same as being a real product. An A record can point at a parking page or a holding server just as easily as at a SaaS app. This is exactly how our 86.5% DNS-liveness figure and the external finding that ~61% of .ai websites are placeholders coexist without contradiction: they measure different layers. Most .ai roots answer in DNS (86.5%); a large share of what they answer with is still a placeholder page (≈61% by content audit). The namespace is live but not yet, in the majority, productive — which is the whole story of .ai in one pair of numbers.

Our June 2026 follow-up takes this DNS pass much further. ".ai After the Gold Rush" resolves A, MX, NS, and TXT records for the entire .ai root population — finding that 94.3% resolve but only 48.5% publish any real-use signal (mail, SPF, or a SaaS verification token), 20.4% carry a verification token at all, and ~9% sit on for-sale nameservers. It is the direct, first-party measurement of "active vs. placeholder" that this section can only approximate.

The Hype Wave Echo: AI Buzzwords Written in DNS

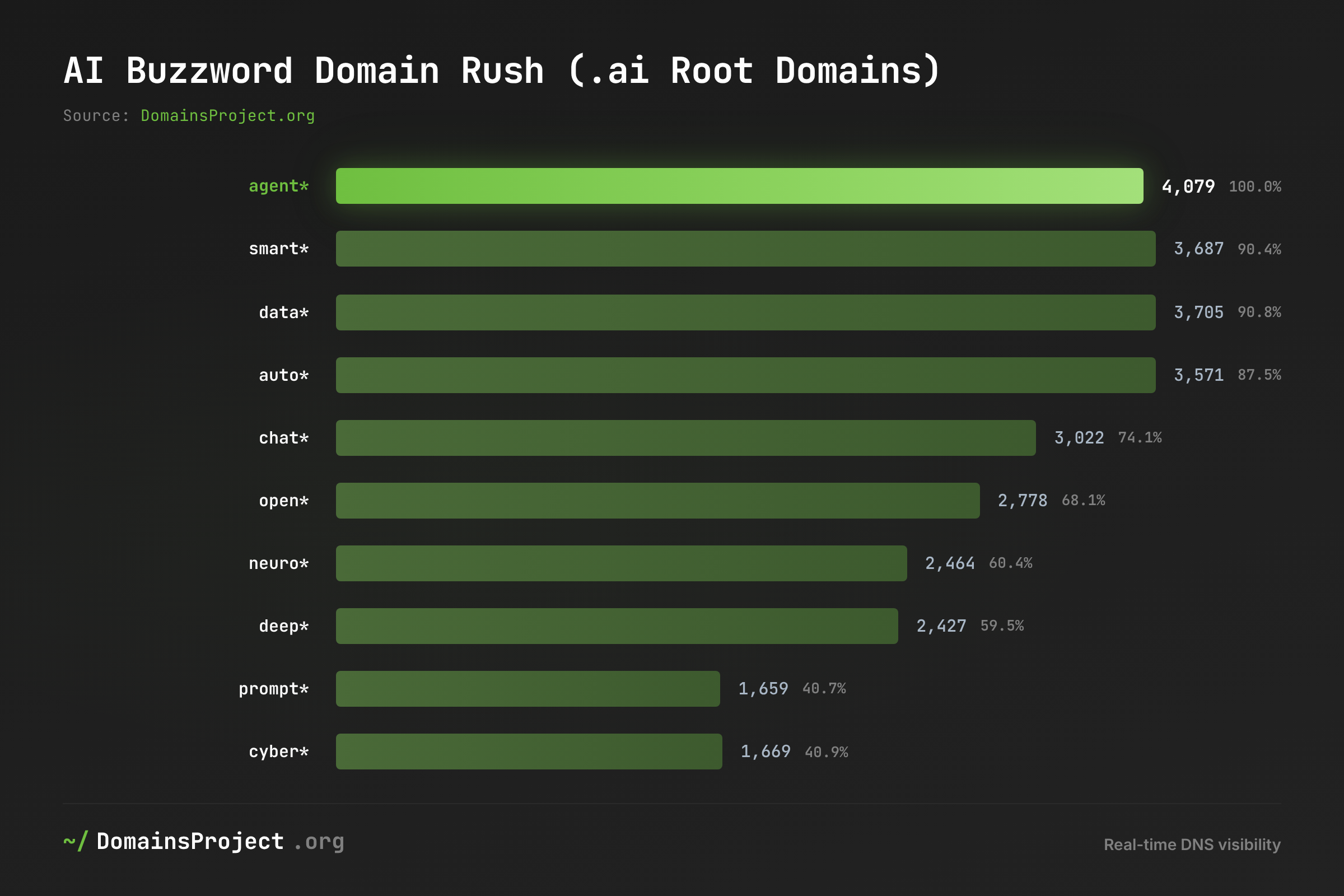

Every phase of the AI boom leaves a fossil record in domain registrations. We counted root .ai domains starting with each major AI buzzword to map how hype cycles translate into namespace claims.

AI Buzzword Domain Rush

| Buzzword | Root Domains | Era | Signal |

|---|---|---|---|

| agent* | 5,681 | 2025-26 | Agentic AI is the current wave |

| data* | 4,073 | 2015-present | Foundational — every AI company touches data |

| auto* | 4,059 | 2018-present | Automation and autonomous systems |

| smart* | 4,001 | 2015-present | Perennial — "smart" never goes out of style |

| open* | 3,633 | 2020-present | Open-source AI movement |

| chat* | 3,231 | 2022-23 | The ChatGPT registration rush |

| deep* | 2,644 | 2016-22 | Deep learning's peak brand value |

| neuro/neural* | 2,310 | 2015-21 | The deep learning era's legacy |

| cyber* | 1,865 | 2020-present | AI + security intersection |

| prompt* | 1,864 | 2023-24 | The prompt engineering wave |

| cloud* | 1,823 | 2018-present | Infrastructure layer |

| robo/robot* | 1,794 | 2016-present | Physical AI |

| vibe* | 1,628 | 2025-26 | The vibe coding phenomenon |

| agentic* | 1,512 | 2025-26 | The agentic sub-wave specifically |

| quantum* | 1,391 | 2022-present | Quantum + AI speculation |

| voice* | 1,040 | 2019-present | Conversational AI |

| gpt* | 996 | 2022-24 | GPT-branded everything |

| vision* | 631 | 2018-present | Computer vision |

| llm* | 557 | 2023-24 | Large language model era |

| mcp* | 414 | 2025-26 | Model Context Protocol (newest) |

| rag* | 333 | 2024-25 | Retrieval-augmented generation |

| copilot* | 144 | 2023-24 | AI assistant branding |

| diffusion* | 23 | 2022-23 | Image generation niche |

| transformer* | 14 | 2020-22 | Too technical for branding |

"Agent" has tightened its grip as the dominant AI keyword in .ai root domains. With 5,681 registrations — up from 4,079 a quarter earlier, including 1,512 "agentic*" domains specifically — the agentic AI wave is now decisively the single largest buzzword category in the .ai namespace, and the fastest-growing. This maps directly to the industry shift: Y Combinator's recent batches run heavily toward agentic AI companies, and the "agent" subdomain prefix appears across .ai platforms (agent.company.ai), suggesting production deployment of agent-based architectures.

The "vibe coding" trend has claimed 1,628 .ai root domains — up from 1,393 — a remarkable footprint for a term that entered mainstream discourse only in early 2025. Domains like vibecoder.ai, vibedev.ai, and vibe2code.ai show speculators racing to claim the term before the window closes. But the vibe coding phenomenon has a secondary effect on the .ai namespace: AI-assisted coding is lowering the barrier to building software, creating a wave of micro-projects and micro-startups — each of which needs a domain. CircleID reports that this "vibe coding revolution" is actively reshaping domain registration patterns.

MCP (Model Context Protocol) domains grew to 414 root registrations — domains like mcpserver.ai, mcpagent.ai, and mcphub.ai demonstrate how rapidly the .ai namespace absorbs each new technical standard. By contrast, "transformer" — the architecture underlying virtually all modern AI — produced only 14 root .ai domains. The lesson: brandable buzzwords drive registrations, not technical accuracy.

60,724 root domains contain "ai" in the name itself — up from 51,533 — registrants doubling down on the AI signal by putting "ai" in both the domain name and the extension. chatai.ai, agentai.ai, dataai.ai — the redundancy is the point. When you're selling an AI product, you can never say "AI" too many times.

The Namespace Landgrab: Saturation Is Approaching

The .ai namespace is finite, and premium names are disappearing fast. Our dataset reveals how thoroughly the short-domain space has been claimed.

Short Domain Saturation

| Category | Total Possible | Registered | Saturation |

|---|---|---|---|

| 1-character (a.ai - z.ai, 0.ai - 9.ai) | 36 | 36 | 100% |

| 2-character alpha (aa.ai - zz.ai) | 676 | 661 | 97.8% |

| 2-character alphanumeric | 1,296 | 1,255 | 96.8% |

| 3-character alpha (aaa.ai - zzz.ai) | 17,576 | 16,310 | 92.8% |

| 5-char or shorter | — | 170,923 | — |

| Numeric-only | — | 2,794 | — |

Every single-character .ai domain is registered. All 26 letters and all 10 digits — a.ai through z.ai, 0.ai through 9.ai — are taken. The two-character alpha space is 97.8% saturated, with just 15 combinations remaining out of 676. The three-character alpha space has tightened to 92.8% claimed, up two points in a quarter. At current registration rates, the three-character namespace will be fully saturated within months.

We tested every common three-letter English word against the dataset. All 39 we checked — from "the" and "and" to "use" and "new" — are registered. The era of registering a recognizable English word as a .ai domain is effectively over. The remaining inventory is acronyms, creative coinages, and combinations nobody else wanted.

Sector Distribution

| Sector | Root Domains | % of Root Total |

|---|---|---|

| Finance/fintech | 9,156 | 0.78% |

| Marketing/sales | 5,676 | 0.48% |

| Data/analytics | 5,258 | 0.45% |

| Health/medical | 4,650 | 0.40% |

| Code/dev tools | 3,721 | 0.32% |

| Security/cyber | 3,451 | 0.29% |

| Education | 3,191 | 0.27% |

| Image/video/creative | 3,154 | 0.27% |

| Legal | 1,918 | 0.16% |

| Voice/speech | 1,291 | 0.11% |

Counts based on tightened keyword prefix matching against the 1,171,566 root .ai domains; categories are not mutually exclusive and capture naming intent, not verified business activity.

Finance leads the .ai sector distribution with 9,156 root domains — fin.ai, bankai.ai, tradeai.ai, and thousands more. Data/analytics and marketing follow. The pattern mirrors real-world AI adoption: financial services, data tooling, and marketing were the first industries to deploy AI at scale, and their domain registrations reflect it. The legal sector's 1,918 domains — including contract.ai, compliance.ai, and dozens of "legalai" variants — shows even traditionally conservative industries racing to claim .ai real estate.

Advanced AI Terminology: The Technical Frontier

| Term | Root Domains | What It Reveals |

|---|---|---|

| synthetic* | 196 | Synthetic data generation |

| alignment* | 33 | AI safety as branding |

| reasoning* | 33 | The latest model capability |

| finetuning/finetune* | 18 | Model customization |

| guardrail* | 18 | Enterprise AI governance |

| multimodal* | 16 | Next-gen model architecture |

| hallucination* | 13 | The problem everyone's solving |

| embedding* | 8 | Vector search infrastructure |

335 root domains use this advanced AI terminology — technical jargon that would have been meaningless to domain registrants three years ago.

The presence of 335 domains using advanced AI terminology — synthetic data, alignment, reasoning, guardrails — suggests the .ai registrant base has become more technically sophisticated. These read less like speculators grabbing catchy words and more like practitioners registering domains that map to specific technical capabilities and problems. When someone registers alignmentlab.ai or guardrailengine.ai, they likely know exactly what they're building.

The Gold Rush: From Startup Signaling to Industry Standard

The .ai domain didn't become valuable because the TLD is technically superior. It became valuable because it says the right thing at the right time.

The Startup Signal

Over 30% of recent Y Combinator AI startups now use .ai as their primary domain, up from negligible levels before 2022. YC's 2026 batches are roughly 60% AI companies — up from 40% in 2024 — and the .ai adoption rate among AI-focused startups continues to accelerate. Meanwhile, .com's share among YC startups has dropped from 64% in 2020 to under 50% in recent batches.

The economics explain why. A startup called "Acme AI" faces a choice: buy acmeai.com or getacme.com or tryacme.com for $10/year, or buy acme.ai for $90/year and get the exact brand match. 85% of non-.com domain choosers achieve exact brand-name matches, compared to just 54% of .com users who are forced to add prefixes, suffixes, or hyphens. For an AI company, .ai is not just a domain — it's a brand statement that says "this is what we do" without a word of copy.

Who's Building on .ai

The companies using .ai as their primary domain read like a list of the AI industry's most-funded startups:

| Company | Domain | Category | Notable |

|---|---|---|---|

| Perplexity | perplexity.ai | AI Search | 42M+ monthly visits |

| Character.AI | character.ai | AI Companions | 441M+ monthly visits |

| xAI | x.ai | Foundation Models | Merged into SpaceX ($250B valuation) |

| C3.ai | c3.ai | Enterprise AI | NYSE-listed |

| Stability AI | stability.ai | Image Generation | Stable Diffusion creator |

| Jasper | jasper.ai | AI Writing | $1.5B+ valuation |

| Copy.ai | copy.ai | AI Writing | |

| Runway | runway.ai | AI Video | Gen-2/Gen-3 |

| Figure AI | figure.ai | Robotics | Humanoid robots |

| Shield AI | shield.ai | Defense AI | $2.7B+ valuation |

| Pony.ai | pony.ai | Autonomous Vehicles | NASDAQ-listed |

| H2O.ai | h2o.ai | ML Platform | |

| Cohere | cohere.ai | Foundation Models | Enterprise LLMs |

| Inflection AI | inflection.ai | Foundation Models | Pi chatbot |

| Mistral AI | mistral.ai | Foundation Models | European AI leader |

| Together AI | together.ai | Inference Infrastructure | Open-source focus |

The notable holdouts are equally telling. OpenAI uses openai.com (and doesn't even hold openai.ai in our dataset). Anthropic uses anthropic.com (though anthropic.ai resolves). Google DeepMind uses deepmind.google. The largest AI labs — the ones that predate the .ai land rush — didn't need a domain extension to signal their identity. The .ai TLD is a startup phenomenon, not an incumbent one.

The VC Correlation

The .ai registration curve tracks AI venture funding almost perfectly:

| Year | AI VC Funding | .ai Registrations (EOY) | YoY Growth |

|---|---|---|---|

| 2022 | $45B | ~150,000 | 15% |

| 2023 | $55.6B | ~354,000 | 136% |

| 2024 | $110B | ~580,000 | 64% |

| 2025 | $202-259B* | ~950,000 | 64% |

AI VC figures for 2025 vary by methodology: Crunchbase reports $202.3B (full AI stack), broader definitions reach $211B, and the OECD's count — including AI-adjacent firms — reaches $258.7B (61% of all global VC). All sources agree on a 75%+ year-over-year increase. Registration figures are calendar year-end estimates derived from registry snapshot data. The one-million milestone was reached in early January 2026.

When venture capital deployed $200+ billion into AI in 2025 — a 75%+ year-over-year increase — .ai registrations surged in lockstep. Every new AI startup needs a domain. When $200 billion is chasing AI companies, $90/year for the perfect domain is a rounding error on the cap table.

Anguilla's Windfall: $93 Million from Two Letters

The .ai story is also a development economics story. Anguilla is a British Overseas Territory with a GDP of approximately $400 million, an economy built on tourism and financial services, and a population that could fit inside a small stadium. Now it's earning more from domain registrations than from most other revenue sources combined.

Revenue Timeline

| Year | Estimated .ai Revenue | Share of Government Revenue |

|---|---|---|

| 2018 | ~$2.9M | ~5% |

| 2022 | ~$10M | ~8% |

| 2023 | ~$32M | ~22% |

| 2024 | ~$39M | ~25% |

| 2025 | ~$93M | ~47% |

| 2026 (projected) | ~$96.4M | ~45% |

Anguilla's .ai revenue has grown 32x since 2018, from $2.9 million to roughly $93 million in 2025. On a per-capita basis, that's approximately $6,450 per resident — from domain registrations alone. The revenue is funding airport expansion, hurricane-resilient infrastructure, abolition of property tax for residents, and free healthcare for children and the elderly. The 2026 government budget projects EC$260.5 million (~$96.4 million) in domain registration receipts — a figure that does not yet fully account for the March 2026 price increase.

The Management Shift

For nearly 30 years, .ai was managed by Vincent Cate, an American technologist who was personally delegated the TLD by Jon Postel in the mid-1990s. In January 2025, management transferred to Identity Digital, a major registry operator. The transition brought immediate changes: the number of accredited registrars grew from roughly 40 to 148, a Namecheap expired-domain auction channel launched, and — critically — Anguilla's revenue share increased from 75% to 90% of registration fees.

Identity Digital's takeover professionalized .ai's infrastructure while increasing Anguilla's cut. The March 2026 price hike — raising wholesale prices by $20/year (from $70 to $90) — was the first pricing action under the new management. At current registration volumes, the increase will generate an estimated additional $20 million in annual revenue — pushing potential 2026 receipts well above the government's conservative $96.4 million projection.

The Governance Question

Anguilla's Premier has publicly warned against over-reliance on .ai revenue. The concern is well-founded. When a single income stream accounts for nearly half of government revenue, any disruption — a registration slump, a pricing backlash, or an AI market correction — becomes a fiscal crisis. Anguilla is, in effect, running a sovereign wealth strategy with a two-letter domain extension as the underlying asset.

The Hacked ccTLD Playbook: .tv, .io, and .co

Anguilla isn't the first small territory to strike gold with a domain extension. The playbook is well-established — and the outcomes are mixed.

ccTLD Monetization Scorecard

| TLD | Territory | Population | Annual Revenue | Revenue per Capita | Key Risk |

|---|---|---|---|---|---|

| .ai | Anguilla | 14,410 | ~$93M | ~$6,450 | AI hype dependency |

| .tv | Tuvalu | 11,312 | ~$10M | ~$884 | Low negotiating leverage |

| .io | Brit. Indian Ocean Terr. | 0 (military) | ~$42M | N/A | Sovereignty transfer |

| .co | Colombia | 52M | Undisclosed | Minimal | None (stable) |

| .me | Montenegro | 620,000 | ~$2.5M | ~$4 | Low growth |

.tv's cautionary tale: Tuvalu leased .tv to a private company in 2000 for $50 million over 50 years — a deal that looked generous at the time but left Tuvalu capturing a fraction of the TLD's true value for two decades. When the contract expired, Tuvalu renegotiated and doubled its revenue to roughly $10 million/year. Anguilla's 90% revenue share under Identity Digital is a far better deal, but it took 30 years to get there.

.io's existential crisis: The British Indian Ocean Territory sovereignty treaty was signed on May 22, 2025, transferring the Chagos Archipelago to Mauritius (with Diego Garcia leased back to the UK for 99+ years). If the ISO eventually removes the "IO" country code from its standard, ICANN policy creates a pathway for phased retirement of the .io TLD — a process that would take 5+ years and affect approximately 1.6 million registry registrations (13.8M observed hostnames in our dataset). ICANN addressed the situation directly in a November 2024 blog post, noting that "it is not a foregone conclusion that a change in sovereignty will result in a change to the .io domain." The former Yugoslavia's .yu persisted for years after the country dissolved before its eventual 2010 retirement, and ICANN's own precedent suggests that retirement is far from automatic. The ISO has not yet acted on the "IO" code. The risk is strategic uncertainty, not imminent technical threat. For startups choosing between .ai and .io today, .ai carries less geopolitical risk.

.co's quiet success: Colombia opened .co to worldwide registration in 2010. Twitter (t.co), Google (g.co), and Amazon (a.co) validated it early. It reached 1.5 million registrations by 2013 and remains stable. .co proves that a hacked ccTLD can achieve lasting adoption — but also that growth plateaus once the initial wave of early adopters passes.

The pattern is clear: hacked ccTLDs generate windfalls, but the windows are finite. .tv's best years were the early 2000s. .io's peak growth was 2015-2020. .co stabilized years ago. .ai is in its explosive growth phase now — but every precedent suggests this phase doesn't last forever.

Bubble or Foundation? Reading the Signals

The .ai domain market sends contradictory signals. The bulls point to real companies, high renewals, and accelerating adoption. The bears point to parked pages, speculative flipping, and hype-dependent demand. Both are right.

The Bull Case

The 90% renewal rate is the strongest signal that .ai adoption is durable, not speculative. Domain investors let speculative registrations expire when they don't flip. A 90% renewal rate means the vast majority of .ai registrants are keeping their domains year after year — paying a premium to do so. This is retention behavior, not speculation behavior.

Institutional adoption is accelerating. Two NASDAQ-listed companies (C3.ai, Pony.ai) use .ai as their primary domain. Multiple unicorns — Perplexity, Character.AI, Jasper, Shield AI — have built their brands on .ai from inception. This isn't hobbyist experimentation — it's a structural shift in how AI companies brand themselves.

Our dataset shows real infrastructure behind a meaningful slice of .ai domains. 1,202 .ai domains run 100+ subdomains each. The 87,628 api. subdomains and 76,382 app. subdomains in our crawl point to production services rather than speculation — though, as the methodology notes, the headline subdomain-to-root ratio of 2.54:1 is inflated by hosting-panel boilerplate, so the production signal is best read from the api/app/dev prefixes specifically, not the raw ratio.

The Bear Case

61% of active .ai websites are placeholders or parked pages. A Dataprovider analysis in October 2024 found that placeholder .ai domains surged 2,271% in a single year. 88% of these placeholders were managed by a single company's affiliates. This is classic speculative domain parking — registrants betting on future appreciation, not building real websites. Beyond the parked domains, just 23% are business/e-commerce sites and 11% are content sites.

Aftermarket prices have reached levels that only make sense if AI hype continues indefinitely. bot.ai selling for $1.2 million and fin.ai for $1 million implies buyers expect .ai domains to appreciate further — or that the AI companies buying them have more venture capital than pricing discipline. When a domain extension's aftermarket grows 13x in two years, some of that is fundamentals and some of it is mania.

Anguilla's March 2026 price hike tests price elasticity. A 29% increase in the annual wholesale rate — from $70 to $90 — on an already-premium TLD is aggressive. If the renewal rate holds at 90%, the hike was well-calibrated. If it drops even a few points, Anguilla's $93M revenue stream contracts.

.ai's abuse profile is worsening. Spamhaus's 2025 Domain Reputation report placed .ai in its Top 20 worst TLDs for the first time, at rank #19. The TLD's premium pricing had previously acted as a natural spam filter — but as .ai becomes mainstream and registration infrastructure scales under Identity Digital, the abuse floor is rising. This is an early warning, not a crisis — .ai abuse rates remain far below notorious TLDs like .top and .xyz — but the "pristine namespace" argument has weakened.

The Verdict

.ai is a durable trend with speculative froth on top — and the froth is getting more expensive to maintain. The foundation — real companies, high renewals, accelerating startup adoption, 1,202 platforms with 100+ subdomains — is sound. The froth — placeholder-heavy registrations, million-dollar aftermarket flips, 13x aftermarket growth, and 5,681 "agent" domains accumulated across the hype cycle — will correct. The question isn't whether .ai survives an AI market cooldown, but how much of the current registration base is real versus speculative.

Gartner's 2025 Hype Cycle placed generative AI in the "Trough of Disillusionment" — a recalibration where, as Gartner put it, "interest wanes as experiments and implementations fail to deliver." Less than 30% of AI executives reported that their CEOs were satisfied with AI return on investment in 2024, despite average investments of $1.9 million. That framing sits in tension with the $200+ billion in AI venture funding deployed the same year, suggesting the trough may be more perceptual than financial — or that the money is chasing a smaller number of increasingly expensive bets.

If AI investment eventually pulls back from its $200 billion annual pace, .ai registrations will slow — but they won't collapse. The companies already building on .ai (Perplexity, Character.AI, xAI, C3.ai, Mistral, Together) aren't going anywhere. The domain speculators parking acme.ai and hoping to flip it — they'll let their registrations expire, and the 90% renewal rate will drift toward 70-80%.

The historical precedent supports this reading. .io survived the 2000 dot-com bust, the 2008 financial crisis, and a decade of "are startups over" think pieces. It's still at 1.6 million registry registrations and 13.1 million observed domains in our dataset. .ai has stronger demand fundamentals than .io ever did — but it also has higher expectations priced in.

What's at Stake

The .ai domain boom has concrete implications beyond branding:

- Anguilla's fiscal stability now depends on Silicon Valley's enthusiasm — 47% of government revenue from a single, hype-sensitive income stream is a concentration risk that mirrors .com's dominance of the namespace itself. At $93M/year and rising, the stakes are now higher than any previous ccTLD windfall.

- .ai's 9x price premium over .com creates a two-tier startup naming system — well-funded AI startups get exact brand matches at $90/year while bootstrapped founders are priced out, reinforcing the perception that .ai is a venture-backed status signal

- 86.5% of .ai roots resolve, but only a minority host a real site — our DNS crawl finds ~1.01 million of 1.17 million roots returning a live address, while external content audits put ~61% of those on placeholder pages. The functional .ai namespace is on the order of 450,000 genuinely active sites — the "one million registrations" headline overstates real-world usage by roughly 2.5x

- The namespace is approaching saturation at the premium tier — 100% of single-character, 97.5% of two-character, and 90.4% of three-character alpha domains are registered. The easy names are gone.

- .io's sovereignty crisis makes .ai the default choice for new tech startups — the Chagos treaty (signed May 2025) creates strategic uncertainty that .ai, with Anguilla's stable ISO 3166-1 status, doesn't face

- The March 2026 price hike is the first test of .ai's price elasticity — if renewal rates hold, expect further increases; if they don't, Anguilla's $93M revenue stream contracts

- The "agent" wave has already claimed 5,681 root domains — the speed of namespace absorption for each new AI buzzword (agent, vibe, MCP) suggests that by the time a term goes mainstream, the .ai real estate is already locked up

- Domain speculators face asymmetric downside risk — with aftermarket prices up 13x, wholesale costs rising 29%, and Spamhaus noting increased abuse, the carry cost and reputational risk of speculative .ai registrations are both increasing

What Would Help

1. AI founders: register your .ai domain now, but own your .com too. The .ai premium is worth paying for brand signaling, but .com remains the Internet's default. Defensive registration of both protects against future uncertainty. With the March 2026 price increase now in effect, waiting costs more — and at 97.5% two-character saturation, short domains are effectively gone.

2. Domain investors: the easy money in .ai is already gone. With aftermarket prices up 13x, registration costs rising to $90/yr wholesale, and 90%+ saturation on short domains, the risk/reward has shifted. The best .ai domains are already registered or priced at six figures. Speculating on mid-tier .ai domains at $90+/year carry cost requires increasingly optimistic assumptions about continued AI hype.

3. Security teams: build .ai into your monitoring scope — the abuse floor is rising. Spamhaus flagged .ai in its Top 20 worst TLDs for the first time in 2025. While abuse rates remain low relative to notorious TLDs, the premium pricing filter is weakening as the namespace scales. The .ai TLD statistics page provides current domain counts and namespace context for threat modeling.

4. Anguilla's government: diversify before the window closes. Every hacked ccTLD windfall in history has eventually plateaued. .tv peaked, .io is plateauing, .co stabilized years ago. The current .ai revenue boom is funding real infrastructure — abolishing property tax, launching free healthcare — but the $93M/year run rate assumes indefinite AI enthusiasm. Sovereign wealth fund principles apply: treat windfall revenue as temporary and invest it in permanent capabilities.

5. ICANN and registries: the .ai precedent matters for future ccTLD policy. A two-letter country code generating $93M/year for a territory of 14,000 — while being marketed globally as an industry identifier — challenges the distinction between ccTLDs and gTLDs. As .ai demonstrates, the commercial value of a ccTLD can vastly exceed its geographic purpose. Future delegation and pricing policies should account for this reality.

This analysis was conducted using the DomainsProject dataset, which continuously indexes hostnames across the 1,511 active TLDs in the IANA root zone (Russian-administered TLDs excluded). Dataset counts reflect the June 2026 snapshot and our 9 June 2026 A-record crawl; registry registration figures are sourced from Domain Name Wire, Sherwood News, and Anguilla's 2026 government budget address. Aftermarket data is from DNJournal, Sedo, and Afternic. AI venture funding figures are from Crunchbase and the OECD. Spam data is from Spamhaus Domain Reputation reports. Explore .ai statistics on our TLD statistics page, browse the full TLD dashboard, or access the complete dataset for your own research.